IVR in Banking: Benefits and Use Cases

The banking industry operates on a tightrope, balancing operational costs, ironclad security, and rising customer expectations. While many see IVR as a frustrating relic, a modern, intelligent system is the key to mastering this challenge.

This definitive guide is for banking leaders. We will explore the critical benefits, challenges, and powerful use cases that transform your business phone system from a simple cost center into a strategic asset for growth and customer loyalty.

| Key Metric | Impact on ROI |

|---|---|

| Call Deflection Rate | Directly lowers costs by automating routine inquiries. |

| Average Handle Time (AHT) | Increases agent efficiency. Reduces cost-per-call. |

| Operational Costs | Provides 24/7 service without expensive 24/7 staffing. |

| Customer Retention Rate | Improves customer experience. Reduces churn and protects revenue. |

| Agent Productivity | Frees agents for complex, high-value, or revenue-generating tasks. |

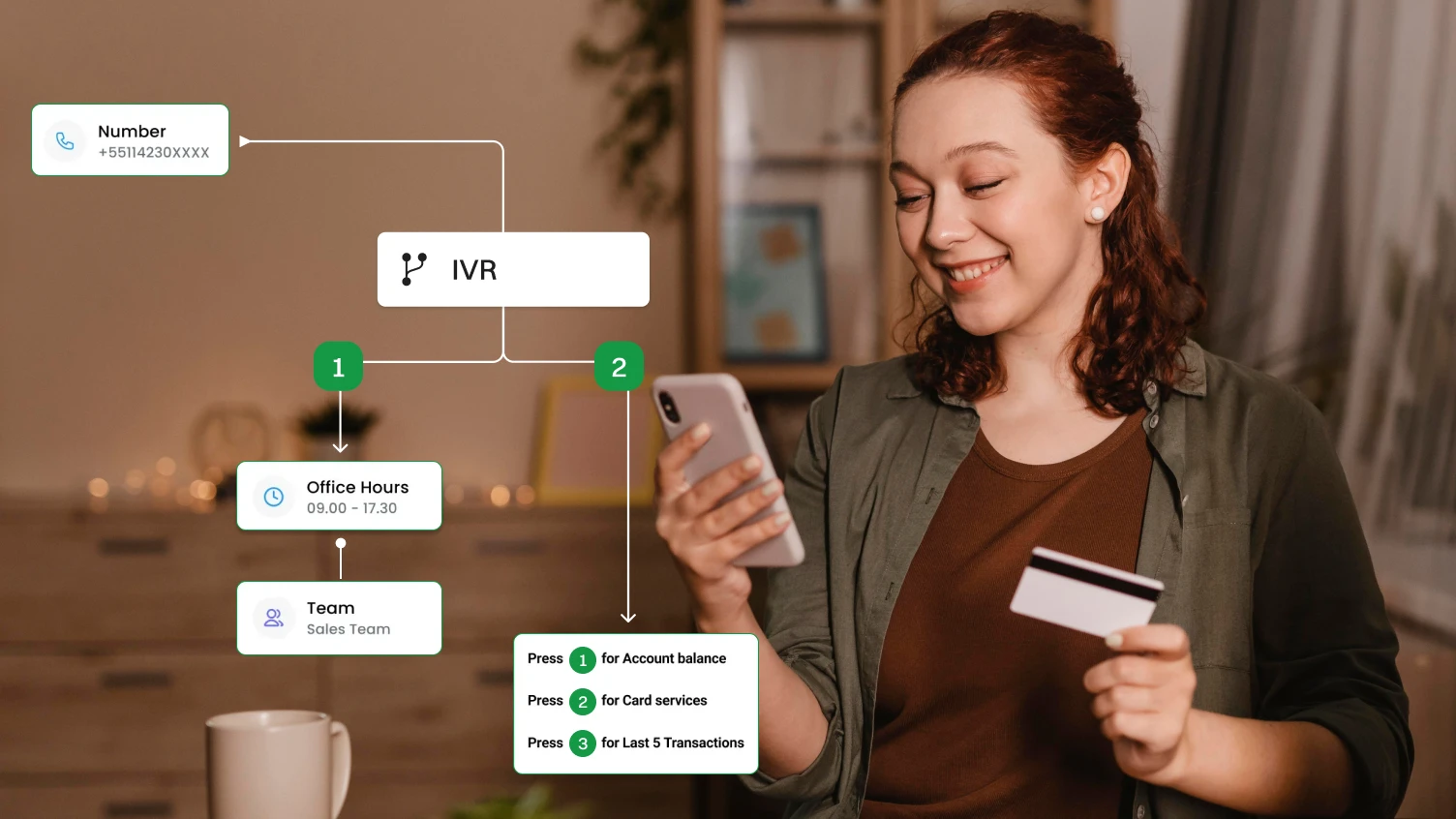

Interactive Voice Response (IVR) is an automated telephony technology that allows customers to interact with a company’s host system through voice and DTMF tones (keypad presses).

Think of it as a digital receptionist that can answer common questions and route calls without a human agent. In the banking sector, this technology is specifically designed to handle financial inquiries and transactions securely.

It enables customers to perform self-service actions like checking balances, making a bill payment, or getting an application status update, 24/7. The primary goal of IVR in banking is to provide instant, secure service while improving operational efficiency.

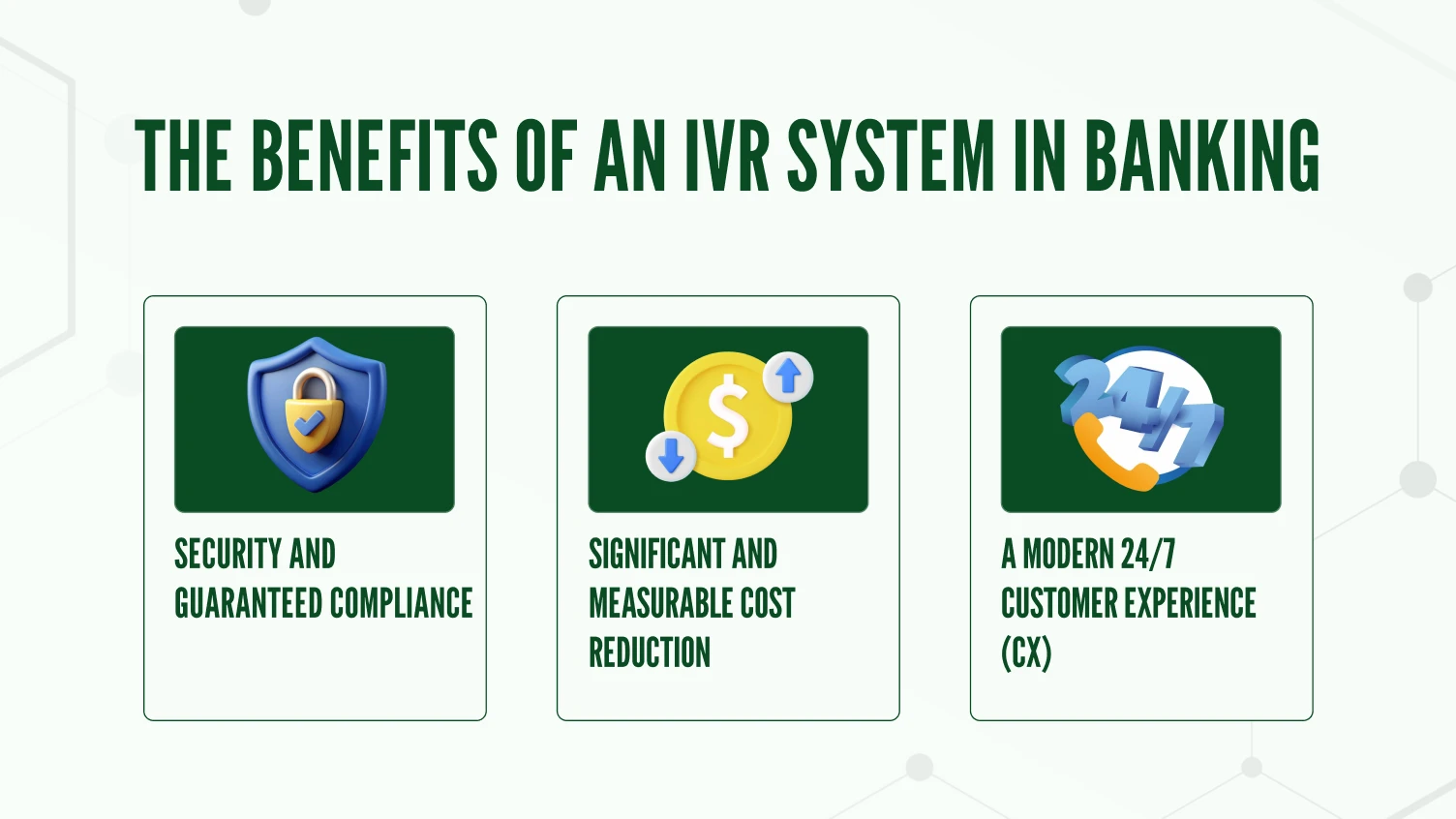

The benefits of IVR extend far beyond financial numbers. A compliant IVR in a banking system improves security and customer satisfaction. It transforms the contact center from a cost center into a strategic asset for the entire financial institution.

Security is the most important pillar for any financial institution. A modern IVR in banking is designed with security as its foundation. It helps banks meet strict compliance standards like PCI-DSS.

For a credit card payment, the system uses DTMF masking. The customer enters their details on their keypad. The information is hidden from the agent and the call recording. Voice biometrics offers an even stronger security layer. This technology identifies a customer by their unique voiceprint.

This is far more secure than PINs or personal questions. It provides a fast and secure authentication process. It prevents fraud while improving the customer experience. A secure business phone system is not optional. It is essential.

An intelligent IVR in a banking system delivers substantial cost savings. It optimizes contact center operations and helps reduce costs. The main way it achieves this is through call containment.

The automated system can handle a high volume of routine customer calls. This includes requests for an account balance or transaction history. Automating these simple queries significantly reduces the call volume to the live agent team. This lowers operational costs directly.

This efficiency also reduces waiting times for customers who do need to speak with a person. When agents are freed from repetitive tasks, they have more time for complex issues. This improves their job satisfaction and lowers expensive staff turnover in the call center.

Today’s customers expect instant service. A well-designed IVR in a banking solution meets this demand. It is a critical tool to improve customer loyalty. The most powerful benefit is 24/7 availability.

Customers can check their application status or report a lost or stolen card at any time. A customer calling late at night about a lost card gets immediate help from the automated system. This is a powerful customer experience.

Personalization further enhances this journey. When the IVR integrates with a bank’s CRM, it can offer a tailored greeting. Instead of a generic message, it can say, “Hello David, are you calling about your recent loan application?” This shows the customer the bank knows them. It makes the customer feel valued.

For any financial institution, technology adoption requires careful planning and due diligence. This checklist helps ensure your IVR in banking solution meets critical security and compliance benchmarks. Use it to evaluate any system provider or your current call center software.

III. Consent Management: Does the IVR technology track and manage customer consent for any outbound call? This is essential for complying with regulations like the TCPA.

III. Unsolicited Outbound Calls: Using the IVR in banking or its auto dialer for marketing without express customer consent. This can lead to heavy fines.

A modern IVR in banking performs many functions that improve efficiency and security. Here are 11 essential use cases that show the power of a modern interactive voice response system in the banking sector.

Handling account inquiries is the most frequent use case for IVR in banking. Customers call the VoIP phone system to check account balances or hear recent transaction history.

Simple automation provides instant answers. It removes a huge burden from the contact center, empowering customers with 24/7 access to their information. The process greatly reduces call volume and operational costs.

Secure card management provides critical 24/7 support. A customer can activate a new credit card. They can also report lost or stolen cards immediately. When a card is reported lost, the automated system can instantly freeze the account to prevent fraudulent activity.

It then informs the customer that a replacement card is on its way. The response system offers vital security and peace of mind.

Automating application status updates for loan applications reduces inbound calls to specialized departments. An applicant can call the IVR in the banking system for a real-time update. They provide their application number to the automated system.

A self-service option saves valuable time for both the customer and the bank’s loan officers. It makes the entire loan or credit card application process more transparent and efficient.

For customers needing in-person services, the IVR provides quick and easy information. The IVR in banking can use the caller’s phone location or ask for a postal code. The system provides the address and operating hours of the nearest branch or ATM. It can deliver this information through a clear voice response or send a text message with details for later reference.

PCI-compliant bill & loan payments feature builds trust through secure transactions. The system lets customers make a bill payment safely over the phone. A voice agent guides the customer to enter payment details using their keypad.

DTMF masking technology ensures sensitive information is hidden from the live agent and the call recording. Protecting customer data is essential for PCI-DSS compliance and is a core function of the IVR in banking.

This use case empowers customers with more control over their daily banking. The IVR in banking allows for the secure transfer of funds between a customer’s own accounts. The system first authenticates the user with a secure method.

It then confirms all transaction details before processing. A common example is moving funds from a savings account to a checking account to cover an upcoming payment.

Proactive fraud alerts can stop potential fraud before it escalates. The IVR in banking can place a critical automated outbound call to a customer if it detects a suspicious transaction.

For example: “We have detected a charge of $500. Was this you?” The customer can confirm or deny the transaction instantly using their keypad. This immediate interaction is a powerful security tool for any bank.

A smart IVR acts as an efficient digital receptionist. It uses speech recognition to understand a customer’s intent from their natural language. If a customer says, “I want to talk about a home loan,” the system routes the inbound call directly to the mortgage department.

Bypassing the main IVR menu options connects the customer to the right live agent faster, improving the customer experience.

With proper customer consent, this feature can improve collections. The IVR in banking can place an automated call to remind customers about an upcoming loan payment, including payday loans, or credit card due date.

Proactive communication helps reduce late payments. It improves the bank’s cash flow. The outbound call feature is a valuable tool for financial institutions wanting to reduce delinquency rates.

Gathering immediate customer feedback provides valuable insights. After a customer speaks with a live agent, the system can automatically transfer them to a short survey. The process gathers immediate feedback on agent performance and overall service quality.

Banks can use this data to identify areas for improvement. It is an essential tool for continuously enhancing the customer experience.

Automating the appointment scheduling process streamlines a key customer interaction. The IVR solution allows customers to book a phone or in-branch appointment with a specialist. It is very useful for complex needs, like a new mortgage application.

The automated system can check calendars and offer available time slots. It is convenient for the customer and reduces administrative work for bank staff.

Call & Contact Center

Sep 19, 2025

Read More

The true power of an IVR in banking is unlocked through integration. A standalone phone system has limited value. It is just an isolated menu. It must connect to your core banking software to be truly effective. This is achieved through modern Voice APIs.

Core Banking Platform Integration: This connection is essential. It allows the IVR in banking to pull real-time data. This includes accurate account balances, transaction history, and loan application statuses. Without this link, the IVR cannot provide useful information.

CRM Integration: Connecting to a CRM like Salesforce or Microsoft Dynamics enables true personalization. The IVR knows who is calling. It knows their history with the bank. It uses this information to provide a better, faster, and more personal customer experience.

Helpdesk Integration: This link allows the IVR in banking to create a support ticket automatically if a customer’s issue cannot be resolved. It ensures no customer query is lost. It provides a smooth handoff to agents with full context.

A compelling real-world example comes from a financial technology campaign in Ghana, where researchers used a Mobile Banking IVR to educate clients. The results were remarkable. The IVR campaign tripled the adoption of mobile banking services, and the effect persisted for months.

More importantly, it drove positive financial outcomes. Clients who interacted with the IVR solution were 8% more likely to repay loans on time, a critical metric for any lending institution.

The system also delivered tangible value directly to the customer. By replacing physical bank trips with IVR-driven digital transactions, clients saw their average transaction costs drop from $4.00 to just $0.16. That’s not just convenience; it’s meaningful savings.

While a modern IVR is a powerful tool, a poorly implemented system can create problems. Banks and financial institutions often face common challenges that can harm the customer experience and reduce ROI.

Recognizing these potential pitfalls is the first step. Implementing the right strategies is the key to overcoming them and unlocking the full potential of your interactive voice response system.

The most common complaint from customers is feeling trapped in an endless IVR menu. They cannot find the option they need. There is no clear way to reach a live agent. The customer presses zero repeatedly in frustration. This creates an extremely negative customer experience.

It can lead to high call abandonment rates. It also damages the bank’s brand reputation. The goal of the IVR in banking is to help customers, not to build a wall around the contact center.

How to Overcome It:

The solution is to design an escape route. A smart IVR should always provide a clear and simple path to a human. Announce the option to reach an agent early in the IVR menu.

For example: “You can say ‘speak to an agent’ at any time.” Furthermore, implement a “fail gracefully” protocol. If the automated system fails to understand a customer’s request twice in a row, it should automatically route the customer’s call to a live agent. This respects the customer’s time and prevents frustration.

Another major challenge is a disconnected system. A customer spends minutes authenticating themselves and explaining their issue to the IVR in banking. Then, when they are finally transferred to a live agent, they are asked for all the same information again.

It is a sign of a system that is not integrated. It creates a disjointed and inefficient journey. It wastes the customer’s time. It also wastes the agent’s time, driving up the Average Handle Time and operational costs.

How to Overcome It:

The key is deep integration with core banking systems. Your IVR solution must have a powerful Voice API. It needs to connect seamlessly with your CRM (like Salesforce or Microsoft Dynamics) and your core banking platform.

When a customer is transferred, the agent’s screen should automatically populate with the customer’s profile, authentication status, and the reason for their call. This “screen pop” creates a smooth handoff. It allows the agent to start solving the problem immediately.

For any financial institution, security is non-negotiable. An older or poorly configured IVR can be a significant security risk. It might handle credit card information in a non-compliant way.

It might have weak authentication methods that fraudsters can exploit. The call recording process might not be secure. A single data breach can lead to massive fines and a complete loss of customer trust. Banks cannot afford to take this risk with their business phone system.

How to Overcome It:

You must choose a system provider that prioritizes security and compliance. Select a platform that is certified PCI-DSS Level 1. This is the highest level of security for handling payment data. Ensure the system uses DTMF masking for all sensitive data entry.

Go beyond simple PINs for authentication. Use modern methods like voice biometrics. All data, especially call recordings, must be encrypted both in transit and at rest. Security should be a primary factor in your decision.

An outdated IVR often sounds robotic and impersonal. It offers the same rigid menu options to every single caller. It does not matter if the caller is a new customer or a high-value client of 20 years.

This one-size-fits-all approach leads to poor customer engagement. It makes the bank seem out of touch with modern customer expectations. Customers today expect personalized service, even from an automated system.

How to Overcome It:

Leverage data to create a personalized experience. Through CRM integration, the IVR in banking can greet customers by name. It can anticipate their needs. If a customer’s loan application was recently updated, the IVR can offer information on that topic first.

Use a high-quality text-to-speech engine to provide a natural and professional AI voice agent. Small details like a clear, human-like voice response can make a huge difference in how the customer perceives the interaction and the bank itself.

The technology behind IVR in the banking sector is constantly evolving. Banks that adopt these future trends will have a significant competitive advantage.

Hyper-Personalization and Predictive AI: Future IVR systems will be predictive. They will analyze a customer’s recent activity to predict why they are calling. For example, if a customer’s credit card was just declined, the IVR will proactively offer to help with that issue when they call.

Seamless Omnichannel Journeys: The line between different communication channels will disappear. A customer might start a query on the bank’s mobile app or via live chat. If they need to escalate to a phone call, they can. The IVR and the live agent will have the full history of the interaction. The customer will not have to repeat themselves.

Voice Biometrics as the Standard: Voice biometrics will become the default method for authentication. Asking for PINs and personal information will be seen as outdated and insecure. Customers will simply use their voice to access their accounts. This will make banking over the phone faster and more secure.

A modern IVR in banking is not just a business phone. It is a core part of a bank’s digital strategy. It solves the industry’s main challenges of security, cost control, and customer experience. This interactive voice response IVR technology transforms the first point of contact.

It changes a frustrating menu into a helpful, intelligent assistant. The benefits of IVR are clear and compelling. From compliant payments to 24/7 service, the right IVR solution is essential for growth in the competitive banking sector.

Dialaxy offers a fully compliant, intelligent IVR built for banks and financial institutions. Improve customer service, stay compliant, and maximize ROI with ease.

IVR service in banking is an automated phone system that enables customers to securely manage their accounts and perform transactions using voice commands or keypad inputs.

A common IVR call example is calling your bank, pressing “1” for account services, entering your account number, and hearing your current balance read back to you by an automated voice.

An IVR payment on a bank statement indicates a transaction you authorized over the phone using an automated payment system, rather than online or in person.

Yes, IVR payments are safe when conducted through a PCI-DSS compliant system that uses technology to mask and protect your sensitive card details during the transaction.

SIP is the underlying protocol that enables voice calls over the internet, while IVR is the application that interacts with the caller during that call to provide automated menus and responses.

IVR reports containing data on call volume and customer interactions can be accessed through the administrative dashboard or analytics portal of your IVR system provider.